For more than thirty years, the U.S. has resisted the restructuring, austerity and market forces required to restore the health, competitiveness and potential of its economy.

Extending a long-running policy of neglect, denial, short-sightedness, political expediency and corruption, for the past two years, the Federal Reserve has tried to prop up the increasingly uncompetitive and defective U.S. economy with what amounts to unprecedented amounts of money printing -- still in effect and slated to expand. The government as a whole has increasingly spent beyond its means, doubled down on debt and pushed the limits of inflation risks as it milks the outdated perception of the dollar as a "safe haven" for all it's worth.

The bill is coming due and the table is being set for the biggest currency crisis ever. Almost all of the key ingredients are in place for a crisis of confidence that will threaten to overwhelm all efforts to contain it -- something beyond the magnitude of currency crises that unraveledMexico in 1994, Asia in 1997, Russia in 1998, and Argentina in 1999. The similarities are now beyond disturbing.

What are the key factors?

1) Financial excess: Key measures of financial excess -- a U.S. budget deficit at 10% of GDP, overall credit amounting to as much as 350% of GDP, a projected $100 trillion more in entitlement obligations than the federal government can currently cover, and more than $1 trillion in state pension underfunding -- are now well into the levels that undermined other countries during currency crises and rendered them insolvent, bankrupt or close to it.

2) Diminishing competitiveness: The gift of hindsight now shows that outside of housing and finance, the U.S. economy was hollowing out over the past 30 years. A withering export base and increasingly lopsided growth (as opposed to broad-based, diversified growth across multiple industries) were telltale signs in Mexico, Russia, Thailand and elsewhere that a country would have trouble paying its bills to creditors abroad.

3) Pre-existing economic pain: A high unemployment rate -- roughly 10% and as much as 20% under broader measures -- will limit the willingness of policymakers to make the tough choices needed to get the country's house in order. As they've already demonstrated, politicians are more likely to continue trying to limit the pain and take the easy way out in the shortrun -- borrowing more and printing more money -- instead of taking real steps to demonstrate the country will be able to pay its bills to creditors abroad without devaluing the dollar (in other words, cut back on spending, raise taxes, reform the economy in a way that bolsters export receipts).

4) Heightened political risk: Ahead of the November midterm elections, the U.S. faces a degree of policy uncertainty we haven't seen since the 1930's and arguably since the years leading up to the Civil War (maybe even further back, the currency chaos after the Revolutionary War). The two parties are both historically weak and want to take the U.S. economy in radically different directions -- Democrats, led by President Obama, toward more government control, greater intervention in the economy and higher taxes and Republicans, increasingly pressured by the Tea Party, toward sharply less government, lower taxes and less intervention in the economy. Unusually critical midterm election this November may set a permanent course or lead to policy paralysis. This is the kind of political uncertainty that formed the backdrop to multiple currency crises, including Mexico's 1994 crisis, which preceded presidential elections.

5) Rising rates abroad: Real, stronger growth outside the U.S. is prompting central banks in Canada, Australia, Latin America, China and elsewhere to tighten credit, while the Fed loosens, inflates and all but signals it wants to let her rip and weaken the currency. That means growing downward pressure on the U.S. dollar. It was the raising of short-term rates in the U.S. through the late 1990's that put Mexico, Asia (particularly Thailand) and Russia under pressure to allow their currencies to collapse.

6) Weak and defective financial system: Large numbers of U.S. banks countinue to fail on a monthly basis across the U.S. The federal government recently announced a stealth $30 billion bailout of credit unions highlights lingering problems. It continues to bankroll massive losses at Fannie Mae and Freddie Mac and has effectively nationalized mortgage finance. We still have inadequate disclosure on the true extent of bad loans -- a key wildcard that led to loss of confidence in Asian and other financial crises. We still don't know the full extent of the black hole. Banking guru Meredith Witney expects a new round of top-line pressure on all the big banks over the coming year.

There you have it: Flagging competitiveness, an inflated exchange rate, chronic deficits, ballooning debt ratios, economic stress, heightened political risk and a defective banking sector. These are the ingredients of a currency meltdown.

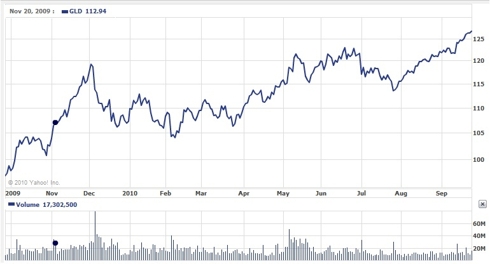

Against this backdrop, as we've seen in past currency crises, speculators eventually take advantage of a status quo they correctly see as unsustainable. They take short positions and/or hedge by buying gold and other protection. Ultimately, central banks can't resist reality and the pressure of the market.

Two additional factors could soon be in play:

1) Capital flight: From elites, top investment funds and banks. The sharp drop of trading volume on U.S. equity markets, heavy inflows into commodity funds, hedges such as gold and even farmland and outflows into overseas markets funds and ETFs may be early omens. There is also growing evidence of human capital flight from the U.S., as the business climate continues to deteriorate and high-skill individuals seek higher after-tax returns from themselves abroad.

2) Violent conflict: The Chiapas Rebellion in Mexico intensified anxiety of the country's management in 1994. Current potential flash points include Iran/Israel/The Middle East, North Korea, the South China Sea and China-Japan.

To paraphrase a previous article:

...if Europe -- also under pressure to take the easy way out of economic underperformance -- joins the U.S. and Japan in the devaluation game, in more earnest than it already has, we'll be in an all-out race to the bottom to export economic depression and inflation -- stagflation -- to one another. Hence the growing lack of confidence in all paper currencies and gold's surging price.

Combined with growing protectionist sentiment and repeated stock market head-fakes, this mess, combined with weakness in the West, Chinese resource hoarding and military buildups, flash points across Asia and the Middle East, is looking more like the early stages and negative feedback loops of the Great Depression, the Weimar Republic and the run up to the Second World War.

Invest (buy gold, silver, other precious metals, farmland-based securities) or divest (out of U.S. currency and dollar-denominated equities and bonds) accordingly.